Cost of living pressures are growing – hitting New Zealanders hard when it comes to financial resilience. However, you can protect yourself by building an emergency fund. That isn’t the easiest though – especially with prices going up all over the place.

Savvy can help, with its suite of powerful tools like boost, salary split and stacks which help you get there slowly but surely.

An emergency fund is there for when things go wrong. It’s something to rely on when we are met with the unpredictable. It is important to realise what an emergency fund isn’t.

It isn’t a savings pot that you can dip into to fund your next holiday or a wardrobe makeover. But it also isn’t something you have to constantly grow...

The first step in establishing an emergency fund is settling on how big it will have to be.

That figure will depend on your situation. If you’re spending a lot on necessities – things such as rent or a mortgage, bills and groceries – your emergency fund will have to be bigger. An easy way to come up with a figure is to base it on your salary.

Having three months of salary in your fund is a good rule of thumb. That might seem like an insurmountable figure – especially if you’re not in the habit of saving in the first place. But it can be done, especially with Savvy’s range of helpful features. All in six easy steps.

-

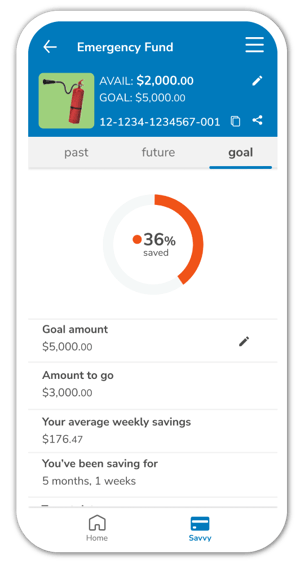

Create a stack

Savvy’s stacks allows you to virtually set aside money in different buckets, so beer money is not mixed with rent. Set one up for your emergency fund which you can then access if the need arises.

-

Set a goal

You can set up a goal along with a deadline when you create a stack. When you select an amount that you want to save Savvy can let you know how much you need to save each week to reach it.

Goals, not just financial ones, are most easily achieved when they are specific, measurable and achievable. Saving three months of salary is specific. Savvy can help measure your progress– no matter how long it takes. -

Automate your savings

The best way to save is to make it automatic. That keeps it out of sight and out of reach, so you won’t be tempted to spend it come payday.

With Savvy there are two ways to do this. You can either set up an automatic transfer into your emergency fund every pay day. Or you can use Salary split which will recognise when your pay has come in and divvy it up across your stacks, just the way you like.

-

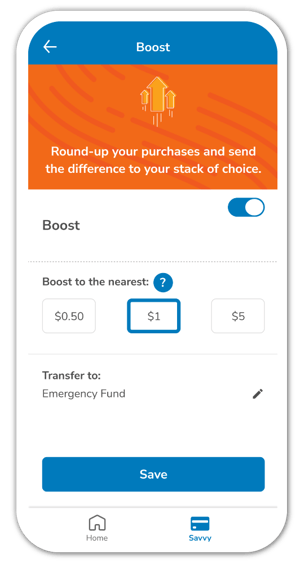

Use boost to get ahead

Boost rounds up your purchases to the nearest 50c, $1 or $5 and then sends the difference to your stack of choice. By sending it to your emergency fund, you can get ahead of your savings deadline.

When you’re saving for the unpredictable, you don’t know when, or even if, it will strike. Getting ahead of schedule will help if an emergency is just around the corner.

-

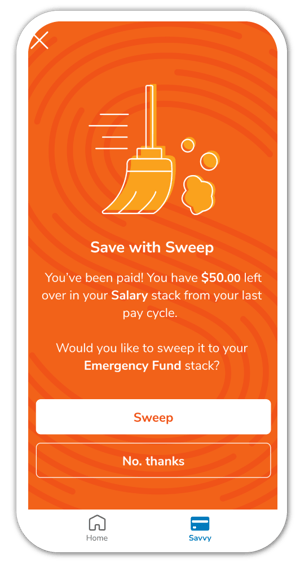

Sweep any extra money

If you’ve got some extra money in your account come payday, Savvy can let you know. You can sweep this into your emergency fund to drive your savings up. -

Bank your windfalls

Rewarding yourself after a promotion, bonus or gift is appealing but putting aside windfalls will help you reach your goal more quickly. While it is nice to indulge a little, by saving most of a windfall you’ll be able to reach your goal sooner.

The best time to start an emergency fund is last year. The second best time is now. So, set your goal, assign your stack and start your emergency fund today.

Share this article

-

The Booster Savvy Scheme (‘Savvy’) is not a bank account and Booster is not a registered bank. Savvy is a managed fund and Booster Investment Management Limited is the manager and issuer of Savvy. Find Savvy’s Product Disclosure Statement, and other important information about Savvy (including a comparison document highlighting some of the differences between Savvy and a bank account) here.