KiwiSaver Guide 2026: Everything Kiwis Need to Know

KiwiSaver is New Zealand's government-initiated retirement savings scheme. You contribute from your pay, your employer adds at least 3.5%, and the government contributes up to $260.72 each year (employer and government contribution eligibility criteria apply).

This guide covers how every part works.

General information only: The information on this page is general in nature. It does not take into account your personal financial situation or goals. Before making investment decisions, consider your own circumstances and, if needed, seek professional financial advice. Read the Product Disclosure Statement before investing.

Key Documents

Before making any investment decisions, please read the relevant disclosure documents: Product Disclosure Statement | Fund Updates | SIPO | Annual Report | Disclose Register

Issuer: Booster Investment Management Limited (BIML) is the manager and issuer of the Booster KiwiSaver Scheme. A copy of the Product Disclosure Statement is available free of charge at booster.co.nz or by calling 0800 336 338.

In This Guide

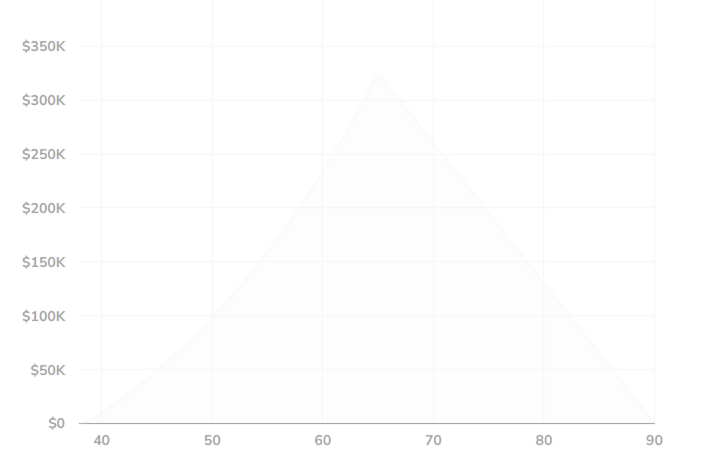

KiwiSaver Calculator

See what your KiwiSaver balance could look like at retirement. Adjust the inputs to match your situation.

*For more information about how the projections are calculated see the Calculator assumptions below.

We’ve calculated your results based on the information you entered, and the assumptions set out under 'Calculator assumptions' below. Our calculator is indended as a guide only and relates to your KiwiSaver account balance.

- Investment rates of return (after fees and tax at 28%) as set by the Financial Markets Conduct Regulations 2014, across four main fund types:

| Fund type | Annual return |

| Conservative | 2.5% |

| Balanced | 3.5% |

| Growth | 4.5% |

| High Growth | 5.5% |

- No savings suspension or withdrawals take place.

- If you’re employed, we’ve assumed an annual salary increase of 3.5% and a 3% employer contribution. The calculator accounts for this salary growth and excludes the Government contribution in any year where the projected income is over $180,000.

- If you're self-employed (or not working), we've assumed your regular annual voluntary contribution increases by inflation (2%) each year.

- Your annual government contribution entitlement amount is received each year, up to a maximum of $260.72. This figure is not adjusted for inflation.

- Fees, tax rates and government contributions are assumed to continue unchanged until you reach age 65.

- All projected balances are in today’s dollar terms (by adjusting for the impact of inflation at 2% per annum).

- After age 65, the graph shows the projected weekly retirement income your lump sum would give you over a 25-year period, assuming a 2.5% annual return (after tax and fees) and a 2% annual inflation adjustment.

- The default contribution rate will increase to 3.5% from 1 April 2026 and 4% from 1 April 2028. You may apply to Inland Revenue to maintain a 3% rate, and your employer may match this. These changes are not included in the estimated lump sum savings total.

- Calculator does not allow the user to adjust the employee contribution amount.

Remember, this result is a guide only and several factors affect the size of your retirement savings and how long this might last in retirement. These include:

- Your choice of fund

- Your contribution rate

- How long you contribute for

- If you are using KiwiSaver to save for a first home

- Other retirement savings and income you may have

- Your expected retirement income levels

- The actual performance of investment markets

If you want advice on your Booster KiwiSaver Scheme account, give us a call on 0800 336 338. Our KiwiSaver specialists can help ensure your fund selection matches your goals.

Not sure which fund type suits your situation? Compare fund types and risk levels below →

What Is KiwiSaver and How Does It Work?

KiwiSaver is a voluntary retirement scheme initiated by the New Zealand government. The Inland Revenue is the central administrator of KiwiSaver. It works through three simple contributions:

- You contribute from your pay,

- Your employer adds at least 3.5% of your salary/wages (eligibility criteria apply)

- The government contributes each year (if you qualify)

From 1 April 2026, the default employer and employee contribution rates changed from 3% to 3.5%. Your contribution rate could remain at 3% if you have applied for a temporary reduction.

Typically you choose which fund your money is invested in, and it stays invested until you reach retirement age (currently 65) or buy your first home. There are also a few select situations where you may be able to withdraw your funds early, such as if you are in significant financial hardship.

KiwiSaver started in 2007 to help New Zealanders save for retirement. As of 2026, over 3 million Kiwis are members. The scheme is voluntary for most people, but employees are automatically enrolled when they start a new job.

How KiwiSaver Works Step-by-Step

- You join or are automatically enrolled

When you start a new job, you're automatically enrolled with one of the government-chosen default providers – like Booster! Booster has been a government-appointed default provider since 2014 – we’re pretty proud of that.

You can also choose which KiwiSaver scheme provider you’d like to join – but if you don’t choose, you’ll start off with one of the default providers. You can also choose to change your KiwiSaver scheme provider – even if you are automatically enrolled with a default one.

You have between weeks 2 and 8 to opt out if you choose not to participate. If you choose to opt out of KiwiSaver, you will need to opt out each time you start a new job. If you want to opt out after the 8 week period you will need to contact Inland Revenue directly. If you have been a KiwiSaver member for 12 months or more you are eligible to apply for a savings suspension of up to a 1-year.

- Contributions from your pay

Your chosen contribution rate (3%, 3.5%, 4%, 6%, 8%, or 10%) is deducted from your before-tax pay each payday. Your employer is responsible for making sure your contribution is deducted and sent into your chosen KiwiSaver account. If you don’t choose a contribution rate, a default rate of 3.5% will automatically be applied.

The default rate rose to 3.5% on 1 April 2026. You can apply to Inland Revenue for a temporary rate reduction if you want to stay at 3% (for up to 12 months).

You can make voluntary contributions at any time – it can be a one-off amount or you can set up a regular payment through your KiwiSaver scheme provider.

- Your employer contributes too

Your employer must put in at least 3.5% (3% if you are on a temporary reduction) of your gross salary, subject to the following criteria;

- The KiwiSaver member must be a contributing employee (meaning you are enrolled in a KiwiSaver scheme and are not on a savings suspension)

- The member must be between 16 and 65 year of age

- The employer isn’t already contributing to a separate eligible registered superannuation scheme for the employeeThis is paid on top of your wages - it’s not deducted from your pay. Your employer’s contribution is part of your overall employment package, and all employers are required to make the contribution (they cannot opt out of their contribution to your KiwiSaver account).

If you’re on a Total Remuneration Package, the above does not apply. Under this arrangement, your employer sets a fixed total pay amount. If you choose to join KiwiSaver, the employer’s contributions are funded from within that total, meaning they are effectively deducted from your pay rather than paid on top of it.The default employer contribution rose to 3.5% on 1 April 2026.

- The government adds their share

If you contribute each year as required, you may receive a government contribution of up to $260.72, subject to the eligibility criteria.

To get the full government contribution, you must contribute at least $1042.86 of your own money each year (between 1 July and the following 30 June), be aged between 16 & 65 and earn less than $180,000 per year. Your employer’s contributions do not count towards the $1042.86 – it needs to come directly from your own contributions. Even if you have not saved the full amount, you still get 25 cents for every dollar you have put in.

- Your money is invested

Your KiwiSaver scheme provider invests your savings in the investment fund you choose. The investments will have different amounts of risk depending on what type of fund you have chosen – it’s important you talk to your KiwiSaver scheme provider about selecting a fund that suits you best. Over time, your investment can generate potential returns that help grow your KiwiSaver savings.

Source: Inland Revenue — KiwiSaver

Recent KiwiSaver Changes

From 1 April 2026, the default employee contribution rate rose from 3% to 3.5%. If you prefer to stay at 3%, you can apply to Inland Revenue for a temporary reduction lasting up to 12 months. This is called the 'opt-down' provision. While every contribution is a good contribution, even a 0.5% increase can make a big difference to your KiwiSaver balance over time.

| Change | Effective Date | What It Means |

|---|---|---|

| Employer contributions for 16 and 17 year olds | 1 April 2026 | Employers must contribute for employees aged between 16-65 |

| Default rate increases to 3.5% | 1 April 2026 | Applies automatically unless you opt-down |

| Opt-down application open | 1 February 2026 | Apply to IRD to stay at 3% for up to 12 months |

| Government contribution changes | 1 July 2025 | Maximum reduced to $260.72 (previously $521.43) |

| Youth eligibility expanded | 1 July 2025 | Members aged 16–17 qualify for government contribution |

| High-income threshold | 1 July 2025 | Members earning above $180,000 taxable income no longer eligible for government contribution |

How to Join KiwiSaver in 2026

Any New Zealand citizen or permanent resident who normally lives in New Zealand can join KiwiSaver. There is no minimum age – parents or guardians can open a KiwiSaver account for their children under 18. If you start a new job and you are between 18 and 65, your employer must automatically enrol you (you can opt out between weeks 2 and 8). From 1 April 2026, if you’re aged 16 or 17, you’ll qualify for employer KiwiSaver contributions if you meet other eligibility requirements.

Who Is Eligible to Join KiwiSaver?

To join KiwiSaver, you must be:

- Be a New Zealand citizen, permanent resident or hold a visa that entitles you to live in New Zealand indefinitely

- Currently be living or normally living in New Zealand

- Have an IRD number

There is no minimum or maximum age to join, though automatic enrolment only applies to employees aged between 18 and 65.

From 1 July 2025, members aged 16 and 17 qualifed for the government contribution (eligibility criteria apply). From 1 April 2026, subject to eligibility, members aged 16 and 17 also receive their employer’s contribution if they are enrolled in KiwiSaver and are making contributions.

Automatic Enrolment for Employees

When you start a new job, your employer is required to automatically enrol you in KiwiSaver if you are aged between 18 and 65. You will be enrolled at the default contribution rate (3.5% from 1 April 2026) unless you choose a different rate. You can change your rate at 3-month intervals, or more frequently if your employer allows it. You have an opt-out window of 2 to 8 weeks from your start date. If you do not choose a provider, you will be allocated to your employer's chosen scheme or a government-appointed default provider.

How to Join KiwiSaver If You're Self-Employed

Self-employed Kiwis can join directly through a KiwiSaver scheme provider like Booster. You will not get employer contributions, but you still receive the government contribution, in part or in full, if you contribute your own money each year (between 1 July and the following 30 June), are aged between 16 & 65 and earn less than $180,000 per year. You choose how much to contribute and when. You can make regular or lump-sum payments directly to your provider.

Joining KiwiSaver If You're Not Working

You can join KiwiSaver directly through a provider, even if you are not currently employed. You can make voluntary contributions whenever you are able or want to. You will still qualify for the government contribution, in part or in full, if you contribute your own money each year (between 1 July and the following 30 June), are aged between 16 & 65 and earn less than $180,000 per year.

Joining KiwiSaver if you’re under 18 years old

If you’re under 18, you can still join KiwiSaver – you’ll just need to get in touch with a scheme provider directly. You cannot join through your employer. If you’re 16 or 17, you need at least 1 legal guardian to co-sign your application. If you’re under 16, you need the consent of at least 1 of your legal guardians, who will contact your chosen scheme provider on your behalf. You cannot enrol yourself.

How to Join the Booster KiwiSaver Scheme

You can join the Booster KiwiSaver Scheme online in a few minutes. You will need your IRD number and some personal details. If you are already a member of a KiwiSaver scheme with another provider, Booster handles the transfer for you.

Join the Booster KiwiSaver Scheme online today

How Much Should I Contribute to my KiwiSaver savings?

You can contribute 3%, 3.5%, 4%, 6%, 8%, or 10% of your before-tax pay. From 1 April 2026, the default contribution rate is 3.5%. To qualify for the full government contribution, you need to contribute at least $1,042.86 per year ($20.05 per week) of your own money between 1 July and the following 30 June, be between 16 & 65 years of age and earn less than $180,000 per year.

| Contribution Type | Rate/Amount |

|---|---|

| Employee (you) | 3%, 3.5%, 4%, 6%, 8%, or 10% of your before-tax pay |

| Employer (minimum) | 3.5% |

| Government (maximum per year) | $260.72 |

Example

If you earn $60,000 and contribute 3.5%, you put in $2,100 per year. Your employer also adds 3.5%, which after tax comes to around $1,750.* That's around $3,850 going into your KiwiSaver account before the government contribution. Add the government contribution, and the total going in is well above what you contribute alone.

*Employer contributions are subject to Employer Superannuation Contribution Tax (ESCT). The rate depends on your income level. Your employer handles the tax - you don't need to do anything.

Can I contribute extra savings on top of my chosen contribution rate?

Yes. In addition to your chosen regular rate, you can make voluntary lump-sum contributions or set up a regular deposit through your provider's website or app, through the ‘Pay Tax’ function on internet banking or directly on IRD’s website using a credit or debit card. These payments will count towards your government contribution eligibility.

How to Change Your Contribution

You can change your contribution rate every three months (or less than that, if your employer agrees). You can make the change by completing a KS2 form and submitting it to your employer, or by changing your rate through your provider's online portal. For Booster members, this can be done through mybooster or through myIR.

Your employer must action the change from your next pay cycle. There is no limit on how many times you can change your rate – it’s a good idea to review your contribution rate regularly or when your life situation changes.

Which Contribution Rate May Suit Your Situation?

The right contribution rate depends on your income, expenses, savings goals, and how far you are from retirement. A higher rate means more goes into your KiwiSaver now, but also less take-home pay today. When setting your contribution rate, consider your full financial picture, including any debts, emergency savings, and other financial commitments.

We strongly encourage people to seek financial advice to determine the best settings for their KiwiSaver account, based on their financial situation and goals. If you are a Booster KiwiSaver Scheme member, you can get financial advice from our in-house team at no extra cost. We can also connect you to an independent financial adviser through our network of hundreds of advisers across the country.

How Does the KiwiSaver Government Contribution Work?

The government contributes 25 cents for every dollar you contribute, up to a maximum of $260.72 per year (eligibility criteria apply). This is sometimes referred to as the ‘member tax credit’.

How to qualify for the full amount:

- Be in New Zealand and aged between 16 and 65

- Contribute at least $1,042.86 per KiwiSaver year (1 July to 30 June). That works out to about $20.05 per week.

- Earn less than $180,000 per year

If you contribute less, the government contributes proportionally less.

Important change from 1 July 2025: Members earning more than $180,000 of taxable income per year no longer qualify for the government contribution.

What Does My Employer Contribute to KiwiSaver?

Your employer must contribute at least 3.5% (3% if you are on a temporary reduction) of your gross pay to your KiwiSaver account subject to the following criteria;

- The KiwiSaver member must be a contributing employee (meaning you are enrolled in a KiwiSaver scheme and are not on a savings suspension)

- The member must be between 16 and 65 year of age

- The employer isn’t already contributing to a separate eligible registered superannuation scheme for the employee

This is paid on top of your salary — it’s not taken from your wages. Some employers contribute more than the minimum.

If you’re on a Total Remuneration Package, the above does not apply. Under this arrangement, your employer sets a fixed total pay amount. If you choose to join KiwiSaver, the employer’s contributions are funded from within that total, meaning they are effectively deducted from your pay rather than paid on top of it.

How Do I Choose a Fund?

Funds typically range from Conservative (lower risk, lower expected long-term returns) to Growth, Agressive and High Growth (higher risk, higher expected long-term returns).

| Fund Type | Typical Mix | May Suit Members Who… |

|---|---|---|

| Cash | 100% cash/bonds | Plan to withdraw within 1-2 years |

| Conservative | 70-80% cash/bonds | Plan to withdraw within 3-5 years |

| Balanced | 50/50 mix | Plan to withdraw within 5-10 years |

| Growth | 70% growth assets | Have 10+ years until withdrawal |

| Aggressive & High Growth | 90% growth assets | Have 10+ years until withdrawal |

Product Disclosure Statements are produced for every fund. These provide full details on the fund, including asset allocation.

A Product Disclosure Statement (PDS) is required to be sent to you before you make a final investment decision. The PDS contains full details on each fund, including asset allocation and a risk indicator as set by the Financial Markets Conduct Regulations 2014. Think of the risk indicator as a guide to how much your balance might move up and down in the short term. The key is matching your fund to your investment timeframe and how comfortable you are with different levels of volatility. You can see all Booster’s funds’ PDS on our website.

Defensive and Conservative Funds

Conservative funds invest mostly in income assets (like cash and bonds). They’re designed to deliver steadier returns with fewer short-term ups and downs. The trade-off? Lower expected long-term growth compared to more growth-focused funds. These funds may suit members who plan to withdraw their money within the next year or so, for example, to buy a first home, and want more stability along the way.

Moderate and Balanced Funds

Balanced funds invest in a mix of growth assets (such as shares and property) and income assets (like cash and bonds), typically in roughly equal proportions. They aim to provide moderate growth with a moderate level of risk. These funds may suit members who are 3 to 10 years from withdrawing their savings and are comfortable with some movement up and down in their account balance in exchange for potential growth.

Growth Funds

Growth funds invest predominantly in shares and property, with a smaller allocation to income assets. Because they focus more on growth assets, your balance may move up and down more in the short term. Over the longer term however, they offer higher expected returns. These funds may suit members with 7 to 10 years until they plan to withdraw their savings.

Aggressive and High Growth Funds

High-Growth funds have the highest allocation to growth assets (such as shares and property), of typically 85-100%. They have the greatest potential for long-term growth, but also the highest level of short-term volatility. This means your balance can rise and fall more noticeably along the way. These funds may suit members with a longer-term, 10+ years investment timeframe.

Socially Responsible (SR) Funds

Ethical investing options that restrict investment in certain industries like fossil fuels, weapons, tobacco and gambling. Booster offers Socially Responsible options across different risk levels. Details of what each fund does and does not invest in are set out in the Statement of Investment Policy and Objectives (SIPO). Choosing to invest in a socially responsible investment fund means you can invest in companies or industries that better align with your personal values.

Important: Past performance is not a reliable indicator of future performance. The value of your investment can go down as well as up, and you may get back less than you invest. Returns are not guaranteed. Before investing, please read the Product Disclosure Statement.

How to Choose the Right Fund

The two most important factors when choosing a fund are:

- Your timeframe — how many years until you plan to use your KiwiSaver

- Your comfort with volatility — short-term ups and downs

In general, the longer your timeframe, the more short-term movement you can afford to ride out in pursuit of long-term growth.

A helpful question to ask yourself is: When do I expect to use this money?

If the answer is 10 or more years away, a Growth, High Growth or Aggressive fund may be appropriate. If you plan to withdraw your savings in the next few years, a more conservative option may be better suited to you. You can change your fund at any time, at no cost — so your choice isn’t locked in forever.

As your life changes, your fund can change too. We strongly encourage people to seek financial advice to help determine the best fund option for their KiwiSaver account, based on their financial goals, timeframe and risk profile. If you are a Booster KiwiSaver Scheme member, you can get advice from our in-house team at no extra cost. We can also connect you with an independent financial adviser through a network of hundreds of advisers across the country.

Booster KiwiSaver Scheme Fund Options

Booster offers 14 funds across the full risk spectrum, from the Enhanced Cash Fund (conservative) through to Geared Growth Fund (aggressive). We also offer Socially Responsible options at multiple risk levels for members who want their investments aligned with specific values. You can view the full fund range, risk indicators, and asset allocations in the Product Disclosure Statement. If your needs change, your fund can too. You can switch funds at any time through mybooster.

Can I Use KiwiSaver to Buy My First Home?

Yes. After 3 years of KiwiSaver membership, you can withdraw most of your balance to use towards a first home purchase. You must keep at least $1,000 in your account.

First Home Withdrawal Requirements

In order to apply for a withdrawal from your KiwiSaver balance, you need to be:

- a KiwiSaver member for at least 3 years

- buying your first home (or in the same financial position as a first-home buyer)

- intending to live on the property

If you are a previous property owner, you may still qualify for a first home withdrawal if you are in the same financial position as a first-home buyer and you have not previously withdrawn your KiwiSaver savings for a first home purchase. Kāinga Ora assesses eligibility on a case-by-case basis.

How Do I Withdraw My KiwiSaver at Retirement?

You can start drawing on your KiwiSaver savings when you turn 65. You can withdraw it as a lump sum, set up regular payments, or leave it invested. There is no requirement to withdraw at 65. Your money can stay invested.

Can I Withdraw KiwiSaver Early for Hardship or Other Reasons?

KiwiSaver is designed to be a long-term savings tool, but there are limited circumstances where you may be able to access your money early. These include:

- significant financial hardship

- serious illness such as a life-shortening congenital condition

- permanent emigration (to countries other than Australia)

Each situation has specific eligibility requirements and documentation, and applications are assessed carefully.

| Reasons for Withdrawal | About this Withdrawal | What can be withdrawn? |

|---|---|---|

| Retirement | You can normally withdraw your savings when you reach New Zealand superannuation age (currently 65)2. You can either withdraw everything and close your account, or keep your savings invested (and invest more if you like) and make partial withdrawals when you want to. You’ll need to withdraw at least $100 each time and if your total balance falls below $1,000, your account will be closed and paid to you. | Your balance1 |

| First home | You can apply to withdraw some of your savings to buy your first home (or land to build your first home on) if you intend to live mainly in that home and it’s located in New Zealand. You’ll need to have been in KiwiSaver for at least three years and not made a first home withdrawal from a KiwiSaver scheme before. You must also leave at least $1,000 in your account. If you’ve owned a home before, you may still be eligible – see www.kaingaora.govt.nz for more information. | Your contributions1, Employer contributions, Government contributions1, Investment earnings |

| Significant financial hardship | You may be able to withdraw some of your savings if you suffer from significant financial hardship as defined in the KiwiSaver Act. The Supervisor will only allow you to withdraw enough money to ease the hardship. You’ll need to show them that you have looked at other ways of finding the money you require. They will also need details of your assets (what you own), liabilities (what you owe), income (what you earn) and expenditure (what you spend). | Your contributions, Employer contributions, Investment earnings |

| Serious illness | You may be able to withdraw your savings if you suffer from a serious illness, as defined in the KiwiSaver Act. You’ll need to provide the Supervisor with medical evidence to help them determine whether you meet the criteria. | Your balance1 |

| Life-shortening congenital conditions | You may be able to withdraw your savings if you suffer from a life-shortening congenital condition, as defined in the KiwiSaver Act. You’ll need to provide the Supervisor with medical evidence to help them determine whether you meet the criteria. | Your balance1,4 |

| Permanent emigration (excluding Australia) | If you permanently emigrate to a country other than Australia, you can apply to withdraw your savings (after at least 1 year) or transfer your savings to an overseas superannuation scheme. You’ll need to provide proof that you have permanently emigrated. | Your contributions3, Employer contributions, Investment earnings |

| Permanent emigration to Australia | If you permanently emigrate to Australia, you can only transfer your savings to an Australian complying superannuation scheme. | Your balance1 |

| Death | In the event of your death, your account balance will be paid to your estate (less any tax and fees), subject to required documentation. | Your balance1 |

| Paying tax on transferred overseas savings | You may be able to withdraw funds to pay New Zealand tax or student loan obligations resulting from overseas superannuation transfers (excluding Australia). Applications must be made within 24 months. | Your contributions, Employer contributions |

| Savings transferred from Australia | If you’ve transferred savings from an Australian superannuation scheme, you can withdraw these when you meet Australian retirement conditions (typically age 60). | Australian transferred savings |

1 Before withdrawing government contributions, we require a statutory declaration stating the periods since joining KiwiSaver when New Zealand was your principal place of residence. You won’t be eligible to receive any government contributions for any period you lived overseas.

2 If you joined KiwiSaver before 1 July 2019 and are age 65 or over, you are able to elect to opt out of the 5-year lockin period and make a retirement withdrawal. If you choose to opt out of the 5-year lock in period, from the date of the withdrawal you will lose any future entitlement to employer and government contributions that you may have received had you not made a retirement withdrawal.

3 Excludes any amount transferred from an Australian complying superannuation scheme.

4 If you make a life-shortening congenital conditions withdrawal you will be treated as if you have reached the New Zealand superannuation qualification age and you will no longer be entitled to government contributions or compulsory employer contributions.

What Fees Do KiwiSaver Scheme Providers Charge?

Most providers charge an annual fund fee (a percentage of your balance) plus fixed administration fees. Fees vary by provider and fund type. Over long periods, fee differences can have a meaningful impact on your balance. The total annual fund charge combines all fees into one percentage.

Types of KiwiSaver Fees

KiwiSaver fees typically include:

- Management fees — a percentage of your balance charged for managing the fund's investments

- Administration fees — a fixed dollar amount or percentage for running your account

- Performance fees — some providers charge an additional fee when a fund exceeds a specified benchmark (not all providers charge this)

The total annual fund charge (sometimes called the total expense ratio) combines all ongoing fees into one percentage so you can compare providers more easily. This is shown in each provider's fund update documents.

How Fees Affect Your Balance Over Time

Even small fee differences compound over decades. A 0.5% difference in annual fees on a $50,000 balance over 30 years could result in thousands of dollars less at retirement, depending on returns and contributions. The Smart Investor tool from the Retirement Commission shows the estimated impact of fees on your projected balance.

Past performance is not a reliable indicator of future performance. Projections are estimates only and depend on actual returns, contributions, and fees.

Comparing KiwiSaver Scheme Provider Fees

When comparing fees, look at the total annual fund charge rather than individual fee components. You can compare fees across all KiwiSaver scheme providers using the Smart Investor tool run by the Retirement Commission. Consider fees alongside other factors such as fund options, service, tools, and investment approach.

Booster KiwiSaver Scheme Fees

Booster's fees are set out in our Product Disclosure Statement. The table below shows estimated total annual fund charges.

| Fund | Total Annual Fund Charge (% p.a.) |

|---|---|

| Default Saver Fund | 0.35% |

| Enhanced Cash Fund | 0.75% |

| Capital Guaranteed Fund | 0.91% |

| Socially Responsible Moderate Fund | 1.10% |

| Moderate Fund | 1.11% |

| Socially Responsible Balanced Fund | 1.22% |

| Balanced Fund | 1.22% |

| Socially Responsible Growth Fund | 1.23% |

| Growth Fund | 1.28% |

| Socially Responsible High Growth Fund | 1.24% |

| High Growth Fund | 1.34% |

| Shielded Growth Fund | 1.35% |

| Socially Responsible Geared Growth Fund | 1.64%* |

| Geared Growth Fund | 1.74%* |

*Interest costs on geared funds apply. See PDS for more details

Important: The fees shown are estimates only. Actual fees may vary. Some funds also charge a member fee of $36 per year and an exit fee. (You will not be charged a member fee if your money has only ever been invested in our default fund. If your money is partially invested in another fund(s) and the balance of your account is over $500, you'll be charged the standard member fee of $36 per year ($3 per month). KiwiSaver balances over $200,000 are also eligible for fee rebates which are tiered depending on the balance. For full fee information, refer to the Product Disclosure Statement.

When choosing a KiwiSaver scheme provider, you may also want to consider fund options, service, tools, and how the provider invests your money. Consider your own situation and what matters most to you.

Full fee details: Booster KiwiSaver Scheme Product Disclosure Statement | Compare providers: Smart Investor

How Do I Switch KiwiSaver Scheme Providers?

You can switch KiwiSaver scheme providers at any time, at no cost. Sign up with your new provider, and they handle the transfer. There is no break in membership and no government paperwork required. The transfer typically takes 10 business days.

Why Switch KiwiSaver Scheme Providers?

Common reasons people switch include seeking better service, fund options, lower fees, access to ethical or socially responsible investing, improved online tools, or a provider that aligns with their values. Switching does not affect your employer contributions, your membership length, or your government contribution eligibility.

How to Switch KiwiSaver Scheme Providers (Step-by-Step)

- Choose your new provider

Compare providers using tools like Smart Investor. Consider fees, fund options, service, and tools.

- Complete the new provider's application

Sign up online or in person or through an adviser. Your new provider will ask for your IRD number and current provider details.

- Your new provider handles the rest

They contact your current provider and arrange the transfer. You do not need to contact your old provider yourself. Your balance transfers across in 10–20 business days.

What to Consider Before Switching

- Fund options available (including ethical and socially responsible investment options)

- Fee structures (total annual fund charge)

- Tools and account access (online portal, app, calculator)

- Customer service and support location (New Zealand based team or overseas call centre)

- Any Service Level Agreements (SLA) in place (how quickly they commit to responding to queries, complaints and applications.

- How your money is invested and the provider's investment approach

- Whether you are in a default fund and have never actively chosen a provider

Switch to Booster KiwiSaver Scheme

Switching to Booster usually only takes a few minutes online. Choose your fund, complete the form, and Booster handles the transfer from your current provider. Your contributions continue without interruption. There is no cost to join, and there is no break in your KiwiSaver membership.

Ready to switch? We handle the paperwork.

Compare providers: Smart Investor (Retirement Commission)

Ethical and Responsible Investing

The Booster KiwiSaver Scheme offers socially responsible investment (SRI) funds across different risk levels. These funds exclude investments in specific industries such as fossil fuels, military weapons, tobacco, and whaling.

Booster also considers Environmental, Social and Governance (ESG) factors when making investment decisions. You can switch to an SRI fund at any time at no cost. Details of what each fund does and does not invest in are set out in the Statement of Investment Policy and Objectives (SIPO).

How to Maximise Your KiwiSaver in 2026

Like all financial investments, KiwiSaver works best when you stay engaged. A few small actions — taken consistently — can make a meaningful difference over time:

- Make sure you receive the full government contribution each year

- Choose a fund that matches your timeframe

- Add voluntary contributions when you can

- Review your settings as your life changes

Because the earlier and more consistently you contribute, the more time compound returns have to work in your favour. Small adjustments today can shape your long-term outcome.

Contribute Enough to Get the Full Government Contribution

The government contributes 25 cents for every dollar you put in, up to a maximum of $260.72 per year. To receive the full amount, you need to contribute at least $1,042.86 between 1 July and 30 June each year. If you’re employed and contributing through your wages, it’s worth checking whether your annual contributions reach this threshold. If not, you can make a voluntary contribution before 30 June. Members earning more than $180,000 of taxable income per year are not eligible for the government contribution.

Choose the Right Fund for Your Time Horizon

Your fund choice should reflect when you expect to use your KiwiSaver savings, not what markets are doing in the short term. If you’re 10 or more years away from accessing your savings, a Growth, High Growth or Aggressive fund may be appropriate. If you plan to withdraw within the next few years, a more conservative fund may better suit your situation. The right fund depends on your personal goals, financial position and comfort with risk. This is general information only - if you’re unsure, consider seeking licensed financial advice.

Make Voluntary Contributions

You can contribute extra to your KiwiSaver account at any time, on top of your regular payroll deductions. There’s no upper limit on voluntary contributions. You can make them through your provider’s online portal or set up a direct debit.

Even small top-ups can:

- Help you qualify for the full government contribution

- Increase the power of compound returns

- Strengthen your long-term balance

Review Your KiwiSaver Account Regularly

It’s worth checking your KiwiSaver account at least once a year. Ask yourself:

- Does my contribution rate still fit my budget?

- Does my fund still match when I plan to use the savings?

- Am I on track to receive the full government contribution?

Life changes - new jobs, pay rises, first homes, retirement planning - can all be good moments to review your settings. Your KiwiSaver account settings should evolve as you do.

Use Booster's Tools to Track and Optimise

If you’re a Booster member, mybooster lets you:

- Check your balance

- Change your fund

- Make voluntary contributions

- Update your details

- View your projected retirement balance

Our KiwiSaver calculator can help you see how different contribution rates and fund types may affect your long-term savings. Projections are estimates only. Actual results depend on market conditions, contributions and fees. Past performance is not a reliable indicator of future performance.

KiwiSaver Contributions Holiday: Taking a Break

If you need to pause your KiwiSaver contributions, you can apply to Inland Revenue for a savings suspension (formerly called a contributions holiday). You must have been a KiwiSaver member for at least 12 months. You can choose how long your suspension lasts between 3 months and 1 year, at which time you can reapply if needed.

What Is a Savings Suspension?

A savings suspension allows you to temporarily stop employee contributions from being deducted from your pay. During the suspension, your employer also stops contributing on your behalf. Your KiwiSaver account stays open, and your existing balance remains invested. You can still make voluntary contributions directly to your provider during a suspension if you choose to.

How to Apply for a Savings Suspension

You apply through Inland Revenue (not your employer or KiwiSaver Scheme provider) online through my IR, or by contacting IRD directly. You choose how long the suspension lasts (minimum 3 months, maximum 1 year). When the suspension ends, contributions restart automatically unless you reapply.

Impact on Your KiwiSaver Balance

While your savings remain invested during a suspension, no new money is added from you or your employer. This may reduce the long-term impact of compound returns. You may also miss out on the full government contribution if your annual contributions fall below $1,042.88. It’s worth considering the longer-term effects before applying.

What Our Members Say

"Such a beautiful service to use. Communication is top tier."

Tracy Faatoafe

Google Review · 7 reviews

"Great Kiwisaver scheme provider"

AndyP

Google Review · Local Guide · 80 reviews

"Friendly and helpful staffs. The onboarding process is pleasant."

Richard Wong

Google Review · Local Guide · 33 reviews

"Overall, Booster delivers on all it promises, and is a refreshing player in the KiwiSaver market."

MoneyHub NZ

Reviews reflect individual opinions and are sourced from Google Business Profile and third-party review sites. Individual experiences may vary.

KiwiSaver FAQs: Common Questions Answered

Who is my KiwiSaver with?

You can check this by logging in to your myIR portal or directly check with Inland Revenue. If you don’t know but have a preferred KiwiSaver scheme provider, you can sign up with them, and they will arrange for your KiwiSaver account to be transferred to them within 10 business days.

Can I have more than one KiwiSaver account?

No. You can only belong to one KiwiSaver scheme at a time. If you switch providers, your full balance transfers across.

What happens to my KiwiSaver account if I lose my job?

Your KiwiSaver account stays open. You won’t receive employer contributions, but you can still make voluntary contributions. The government contribution is based on your own contributions, not your employment status.

Can I withdraw my KiwiSaver savings to pay off debt?

Not directly. However, if your debt means you are unable to meet minimum living expenses, you may be eligible for a significant financial hardship withdrawal.

Are my KiwiSaver savings taxed?

Your contributions come from after-tax pay. Investment returns within your fund are taxed at your Prescribed Investor Rate (PIR) — 10.5%, 17.5%, or 28%, depending on your income.

What happens to my KiwiSaver account if I move overseas?

If you move to Australia permanently, you can transfer your KiwiSaver savings to an eligible Australian superannuation scheme. If you permanently emigrate to another country, you can apply to withdraw your savings after being overseas for at least one year (government contributions cannot be withdrawn).

Can I transfer an Australian super to a KiwiSaver Scheme?

Yes. If you have worked in Australia and have superannuation savings there, you may be able to transfer them to your KiwiSaver account. The transfer is managed between your KiwiSaver scheme provider and your Australian super fund. Tax implications may apply. Contact your provider for details on the process and any conditions.

How do I check my KiwiSaver balance?

Log in to your providers online portal or check directly with them. Booster members can use mybooster or the Booster NZ app.

Why Choose Booster as Your KiwiSaver Scheme Provider?

Booster is 100% New Zealand-owned and operated, and one of six government-appointed default KiwiSaver scheme providers. We offer 14 fund options, including socially responsible investment funds, online account management through mybooster, free calculators, the Booster NZ app and access to financial advisers based in New Zealand.

Kiwi-Owned and Operated

For over 25 years, we’ve been on a mission to help New Zealanders build long-term financial resilience. We’re a New Zealand owned-and-operated financial services company based in Wellington.

Government-Appointed Default Provider

Booster is one of six providers appointed by the New Zealand government to manage default KiwiSaver members. The default provider status is reviewed periodically by the government based on criteria such as investment capability, fees and member service.

Range of Fund Options Including SRI

The Booster KiwiSaver Scheme offers 14 funds across the full risk spectrum, from Capital Guaranteed to Geared Growth. Our socially responsible funds typically restrict investments in specific industries such as fossil fuels, military weapons, tobacco, or whaling. Details of each fund's investment approach, asset allocation, and exclusions are set out in the Product Disclosure Statement and SIPO and you can read more information about our approach to ethical investing here.

Easy Online Management

Manage your KiwiSaver account through mybooster, our online portal. Check your balance, change your fund, make voluntary contributions, update your details and view your projected retirement balance. You can also see your KiwiSaver savings and earnings in the Booster NZ app - available on the Apple App Store and Google Play Store.

KiwiSaver Calculators and Tools

Use Booster’s KiwiSaver calculator to see how different contribution rates and fund types may affect your savings over time. Projections are estimates only and depend on actual returns, contributions, and fees.

Access to Financial Advisers

Booster provides access to financial advisers who can help you make decisions about your KiwiSaver account. Call 0800 336 338 to speak with our Wellington-based team. Booster Financial Services Ltd holds a Financial Advice Provider licence issued by the Financial Markets Authority.

Your KiwiSaver Journey Starts Here

Key Takeaways

KiwiSaver is a voluntary, government-initiated savings scheme that helps New Zealanders save for retirement and their first home.

Your money comes from three sources:

- your contributions,

- your employer's contributions (minimum 3.5%), and

- the government contribution (up to $260.72 per year).

Government and employer contribution eligibility criteria apply.

Your fund choice matters. Match your fund type to your investment timeframe and risk profile. You can change funds at any time.

From 1 April 2026, the default contribution rate rose to 3.5%. You can opt to temporarily reduce your contribution rate down to 3% by applying to the IRD.

Review your KiwiSaver at least once a year. Check your contribution rate, fund type, and whether you are on track for the full government contribution. Small adjustments can make a meaningful difference over time. Whether you are joining KiwiSaver for the first time, switching providers, saving for your first home, or planning for retirement, understanding how KiwiSaver works puts you in a stronger position to make informed decisions about your financial future.

Booster is here to help you build long-term financial resilience - with clear information, practical tools and a team based right here in New Zealand. Booster is committed to helping Kiwis build their savings with clear information, practical tools, and a team based right here in New Zealand.

Official Sources Referenced in This Guide

Looking for a KiwiSaver Scheme provider?

Join online or switch from your current provider. We handle the transfer paperwork.Last Updated: May 2026

Important Information

Issuer: Booster Investment Management Limited (BIML) is the manager and issuer of the Booster KiwiSaver Scheme. The Product Disclosure Statement for the Booster KiwiSaver Scheme is available free of charge at booster.co.nz or by contacting us on 0800 336 338.

Past performance: Past performance is not a reliable indicator of future performance. The value of your investment can go down as well as up, and you may get back less than you invest. Returns are not guaranteed.

General information only: The information on this page is general in nature and does not constitute personalised financial advice. Before making investment decisions, please consider your personal circumstances and, if appropriate, seek professional financial advice. Please read the relevant Product Disclosure Statement before investing.

Licence information: Booster Financial Services Ltd holds a Financial Advice Provider licence issued by the Financial Markets Authority. See our FAP Licence and FI Licence information.

Key Documents

Product Disclosure Statement | Fund Updates | SIPO | Annual Report | Disclose Register